NCERT Solutions for Class 7 Social Science Chapter 8 Banks and the Magic of Finance

The Big Questions

Question 1: What is financial infrastructure, and what does it comprise?

Answer: Financial infrastructure is the system of institutions, services, and technologies that supports the movement and management of money in an economy. It includes banks, ATMs, payment systems, post offices, insurance companies, stock markets, and digital payment platforms. These facilities help people save, borrow, invest, withdraw, and transfer money safely.

Question 2: What are the main functions performed by banks and how do they impact people’s lives?

Answer: Banks perform several important functions, such as accepting deposits, providing loans, transferring money, and offering payment services. They keep people’s savings secure and allow them to withdraw money through ATMs, cheques, debit cards, and online banking.

Banks also provide loans for education, housing, farming, and business activities. In this way, they make financial transactions easier, encourage savings, and support the economic needs of individuals and businesses.

Question 3: How does financial infrastructure contribute to a nation’s progress?

Answer: Financial infrastructure encourages people to save and invest their money. It enables businesses to obtain loans, supports secure digital payments, and makes financial transactions faster and more convenient.

It also helps funds move from people who save money to those who need money for productive activities. When individuals and businesses can access reliable financial services, economic activity increases and contributes to the nation’s development.

Let’s Explore

Question 1: This picture is from a bank. What do you think the people are doing? Ask your family members if they have visited a bank and learn more about the activities there. (Page 194)

Answer: The people in the bank may be depositing or withdrawing money, updating passbooks, filling out banking forms, applying for loans, or using other banking services.

My family members said that they have visited banks to deposit money, withdraw cash, transfer funds, update passbooks, submit cheques, and make payments.

Think About it

Question 1: Why does Navdeep think that saving at the bank is better than keeping cash at home? (Page 196)

Answer: Navdeep thinks that saving money in a bank is better because the money remains protected from theft, loss, or damage. Banks also pay interest on deposits, which allows savings to grow over time. Money kept in a bank can also be accessed easily through ATMs, cheques, or digital banking.

Question 2: Can Navdeep and Rima lend to each other directly without the bank? What could happen in that case? Discuss. (Page 196)

Answer: Yes, Navdeep and Rima can lend money directly to each other, but doing so may involve certain risks. There may be no written agreement, clear repayment schedule, or official record of the transaction. If the borrower cannot repay the money on time, it may lead to misunderstandings or conflict.

Banks follow established rules, maintain proper records, and clearly state the interest rate and repayment conditions. This makes borrowing and lending through banks safer and more organised.

Question 3: How does one track so many transactions of deposits and withdrawals? (Page 198)

Answer: A person can track deposits and withdrawals through a bank passbook or account statement. Each transaction is recorded with its date, amount, and type.

Nowadays, people can also check their transaction history through mobile banking applications, internet banking, SMS alerts, and digital bank statements.

Question 4: Look at the passbook in Fig. 8.7. Observe all the particulars under the expenses (debit) and income (credit). Why is keeping records of financial transactions important? Discuss in the class. (Page 198)

Answer: Keeping records of financial transactions helps people understand how much money they receive, spend, save, deposit, or withdraw. It makes managing a budget easier and prevents confusion about account balances.

Checking records regularly also helps identify calculation errors, duplicate payments, unauthorised transactions, or suspicious activity. Therefore, accurate financial records are important for planning expenses and keeping money safe.

Question 5: Why do companies issue shares, and why do people buy them? Are there any benefits of owning shares? (Page 209)

Answer: Companies issue shares to raise money for expanding their business, purchasing equipment, developing new products, or starting new projects. Instead of borrowing the entire amount, they collect funds from investors by offering them partial ownership in the company.

People buy shares to invest their savings and potentially earn returns. Shareholders may benefit when the market value of the shares increases or when the company distributes part of its profits as dividends. However, share prices may also decrease, so investment in shares involves risk.

Banks and the Magic of Finance Class 7 Solutions (Exercise)

Question 1: What is financial infrastructure? How does it complement physical infrastructure?

Answer: Financial infrastructure consists of institutions, services, and technologies that support money-related activities. It includes banks, ATMs, insurance services, digital payment systems such as UPI, and stock markets.

It complements physical infrastructure because roads, railways, ports, electricity, and communication systems support the movement of people and goods, while financial infrastructure supports the movement of money. Businesses require both physical facilities and financial services to operate and grow effectively.

Question 2: How does having a bank account help people? Should everyone be required to have a bank account?

Answer: A bank account helps people keep their money safe, receive and transfer payments, earn interest, pay bills, and use services such as loans, ATMs, debit cards, and digital payments.

Although having a bank account may not need to be compulsory, everyone should be encouraged to open one. A bank account provides financial security and enables people to participate more easily in the modern economy.

Question 3: What could be the possible advantages and disadvantages of compound interest for savers and borrowers?

Answer: Compound interest benefits savers because interest is earned on both the original amount and the interest already added. As a result, their savings can grow faster over time.

For borrowers, compound interest can become a disadvantage because unpaid interest is added to the outstanding loan amount. If repayment is delayed, the total amount owed may increase quickly and make the loan more expensive.

Question 4: How does financial infrastructure enable the flow of money between households and businesses? Can you think of how the government can facilitate this flow?

Answer: Financial infrastructure enables households to deposit their savings in banks. Banks then use part of these deposits to provide loans to businesses for production, expansion, and other activities. Businesses also pay salaries to households, creating a continuous flow of money.

The government can support this flow by expanding banking services, promoting secure systems such as UPI, regulating banks through the Reserve Bank of India, providing subsidies and credit schemes, and ensuring that financial facilities reach both rural and urban areas.

Question 5: What could be the reason for the higher interest rate earned on fixed deposits as compared to a savings account?

Answer: Fixed deposits usually offer a higher interest rate because the money is deposited for a specific period and cannot be withdrawn as freely as money in a savings account.

Since the bank knows that the money will remain available for a fixed duration, it can use the funds with greater certainty. Therefore, it offers a higher interest rate to the depositor.

Question 6: Sahil received ₹ 10,000 as a prize in a poster-making competition. His father promises to pay him 12 per cent interest per year if he does not spend the amount. After 3 years, how much money would Sahil have?

Answer:

Principal amount = ₹10,000

Rate of interest = 12% per year

Time = 3 years

If the interest is calculated as simple interest:

Interest for one year = 12% of ₹10,000

= ₹1,200

Interest for 3 years = ₹1,200 × 3

= ₹3,600

Total amount = ₹10,000 + ₹3,600

= ₹13,600

If the interest is compounded annually:

After the 1st year:

₹10,000 + ₹1,200 = ₹11,200

After the 2nd year:

12% of ₹11,200 = ₹1,344

₹11,200 + ₹1,344 = ₹12,544

After the 3rd year:

12% of ₹12,544 = ₹1,505.28

₹12,544 + ₹1,505.28 = ₹14,049.28

Therefore, Sahil would have ₹13,600 with simple interest or ₹14,049.28 with compound interest calculated annually.

Question 7: How does the stock market help mobilise the savings of individuals? In what ways do companies benefit by issuing shares to people?

Answer: The stock market allows individuals to invest their savings by purchasing shares of companies. Instead of remaining unused, these savings become available for productive business activities.

Companies benefit by receiving money from investors without taking a traditional loan. They can use the funds to expand production, introduce new products, purchase equipment, or undertake new projects. Thus, stock markets connect people’s savings with the financial needs of companies.

Question 8: How can we balance the convenience of digital payments with the risk of cyber fraud?

Answer: We can use digital payments safely by creating strong passwords, keeping PINs and OTPs private, avoiding unknown links, and verifying the receiver’s details before making a payment.

Bank information should never be shared through suspicious calls or messages. Banking applications should be downloaded only from trusted sources. Any suspected fraud should be reported immediately to the bank and the cybercrime helpline at 1930.

By following these precautions, people can enjoy the convenience of digital payments while reducing the risk of cyber fraud.

Question 9: Ask your family members or neighbours about-

how they save money?

whether they use UPI, ATM or cheques, the kinds of transactions they perform through UPI; do they find UPI better than using cash or not, and why.

if they or their acquaintance have experienced digital fraud, for instance, through a fake call or message asking for bank details. What did they do when they realised it was a scam, and what did they learn from that experience?

Summarise your findings in a table or short report. Share one surprising insight with your class.

Answer:

I asked my family members and neighbours about their saving and payment habits. Most of them save money in savings accounts, fixed deposits, recurring deposits, or small investment schemes.

They use UPI to pay utility bills, purchase groceries, transfer money, recharge mobile phones, and make payments at shops. ATMs are mainly used to withdraw cash, while cheques are used for some large or formal payments.

Most people prefer UPI because it is fast, convenient, and does not require them to carry cash. However, they also said that users must carefully verify the payment details.

One neighbour received a fake message asking for an OTP. The neighbour did not share it, blocked the number, and reported the incident. The experience taught everyone never to disclose banking details, passwords, PINs, or OTPs.

The surprising insight was that many people now use UPI more frequently than cash, even for small everyday payments.

Question 10: Create a Financial Safety Poster.

Design a poster with dos and don’ts of digital banking safety (example, not sharing OTPs, reporting frauds).

Include emergency numbers or websites like https://cybercrime.gov.in or 1930 helpline.

Hang the posters in school corridors or the library.

Answer:

Students can create the poster themselves by including clear digital banking dos and don’ts, along with the cybercrime helpline number 1930 and the official reporting website.

Question 11: Cheques are often used to pay utility bills. Ask your parents to allow you to fill out the cheques for a few monthly payments.

Answer: Students can practise filling sample cheques under parental guidance by correctly entering the date, payee’s name, amount in words and figures, and the account holder’s signature.

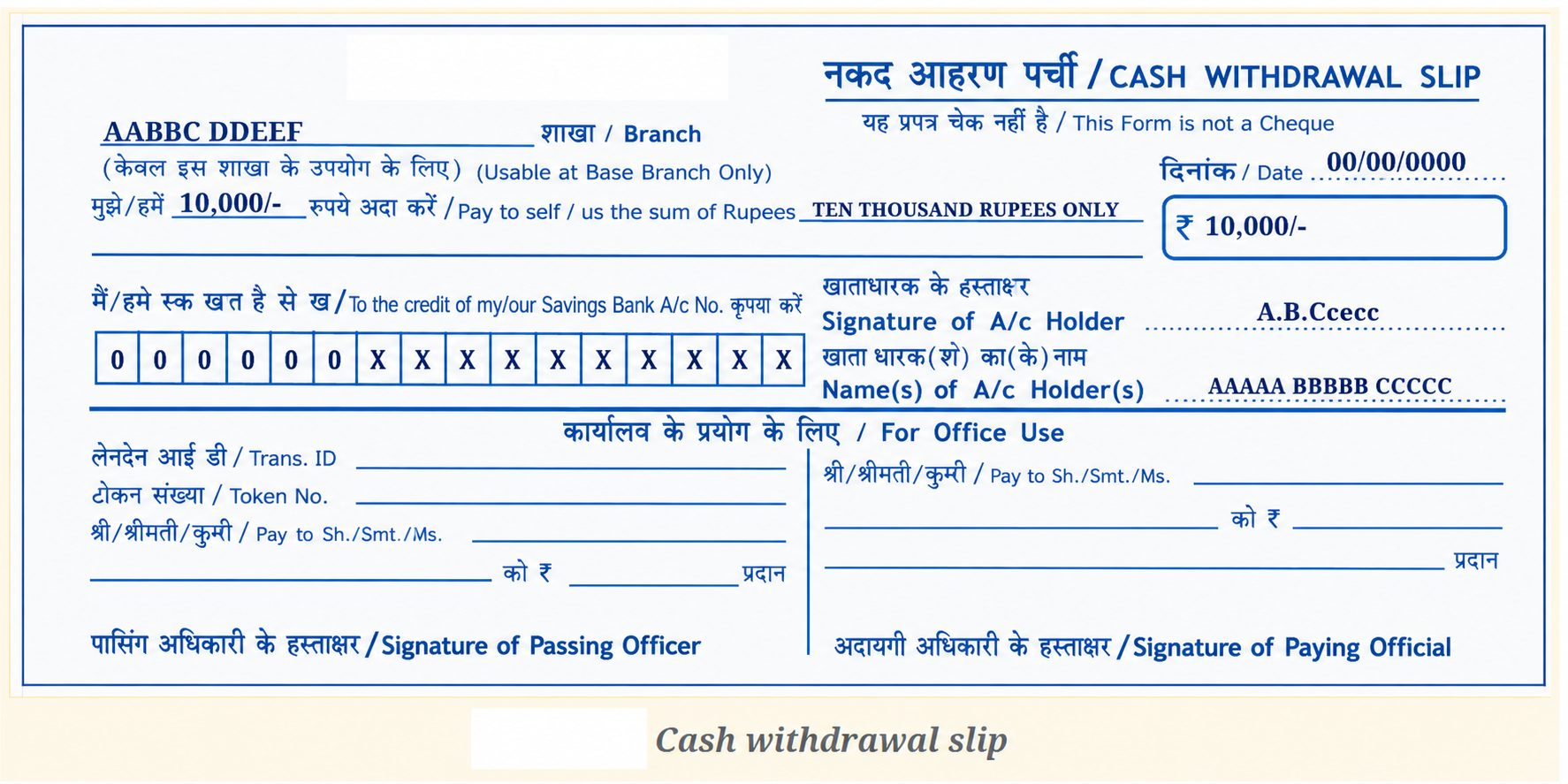

Question 12: Suppose you have to withdraw ₹10,000 from your bank account, how would you fill out the cash withdrawal slip at your bank? Let us try below!

Answer:

To fill out the withdrawal slip, enter the following details:

Date of withdrawal

Name of the account holder

Bank account number

Amount in figures: ₹10,000

Amount in words: Rupees Ten Thousand Only

Account holder’s signature

The completed withdrawal slip should be submitted to the bank cashier along with the passbook, if required. The cashier will verify the details before providing the cash.

Class 7 Social Science Chapter 8 Banks and the Magic of Finance Solutions

Vedantu provides NCERT Solutions for Class 7 Social Science Chapter 8 Banks and the Magic of Finance from Exploring Society India and Beyond Part 2 for the 2026-27 academic session. The chapter explains how financial institutions help people save money, access loans, make payments, invest their savings, and participate in economic activities.

The solutions include easy answers to textbook exercises, picture-based questions, numerical problems, discussions, surveys, and financial safety activities. Students can use them for homework, classroom learning, quick revision, and exam preparation. The downloadable FREE PDF also helps learners study the chapter whenever required.

CBSE Class 7 Social Science Chapter 8 Study Materials

Students can use the Chapter 8 study materials given below to revise important financial concepts, practise additional questions, and strengthen their understanding of banking and finance.

Explore More NCERT Solutions for Class 7 Social Science Chapters

Related Study Material for Class 7 Social Science

FAQs on NCERT Solutions for Class 7 Social Science Chapter 8 Banks and the Magic of Finance – Exploring Society India and Beyond Part 2 (2026-27)

1. What is covered in Class 7 Social Science Chapter 8 Banks and the Magic of Finance?

The chapter explains financial infrastructure, the functions of banks, savings, deposits, loans, interest, digital payments, stock markets, shares, and financial safety.

2. Which book contains Class 7 Social Science Chapter 8 Banks and the Magic of Finance?

Banks and the Magic of Finance is Chapter 8 of the Class 7 NCERT Social Science textbook Exploring Society India and Beyond Part 2.

3. What is financial infrastructure?

Financial infrastructure is the network of institutions, services, and technologies that supports money-related activities. It includes banks, ATMs, payment systems, insurance services, stock markets, and digital banking platforms.

4. What are the main functions of a bank?

Banks accept deposits, provide loans, transfer money, offer payment services, maintain financial records, and help people save and manage their money safely.

5. Why is saving money in a bank better than keeping cash at home?

Money deposited in a bank is safer from theft, loss, or damage. It may also earn interest and can be accessed through ATMs, cheques, debit cards, or digital banking.

6. What is compound interest?

Compound interest is calculated on both the original amount and the interest already added. It helps savings grow faster but can also make loans more expensive if repayment is delayed.

7. Why do fixed deposits offer higher interest than savings accounts?

Fixed deposits usually offer higher interest because the money remains deposited for a fixed period. This allows the bank to use the funds with greater certainty.

8. How does the stock market help companies?

The stock market enables companies to raise money by issuing shares to investors. Companies can use this money to expand production, purchase equipment, or begin new projects.

9. How can students stay safe while using digital payments?

Students should never share their PIN, password, bank details, or OTP. They should avoid unknown links, verify payment details, use trusted applications, and report suspected fraud immediately.

10. Where can students download Class 7 Social Science Chapter 8 solutions?

Students can download the FREE PDF of NCERT Solutions for Class 7 Social Science Chapter 8 Banks and the Magic of Finance from Vedantu for easy learning, homework, and exam revision.